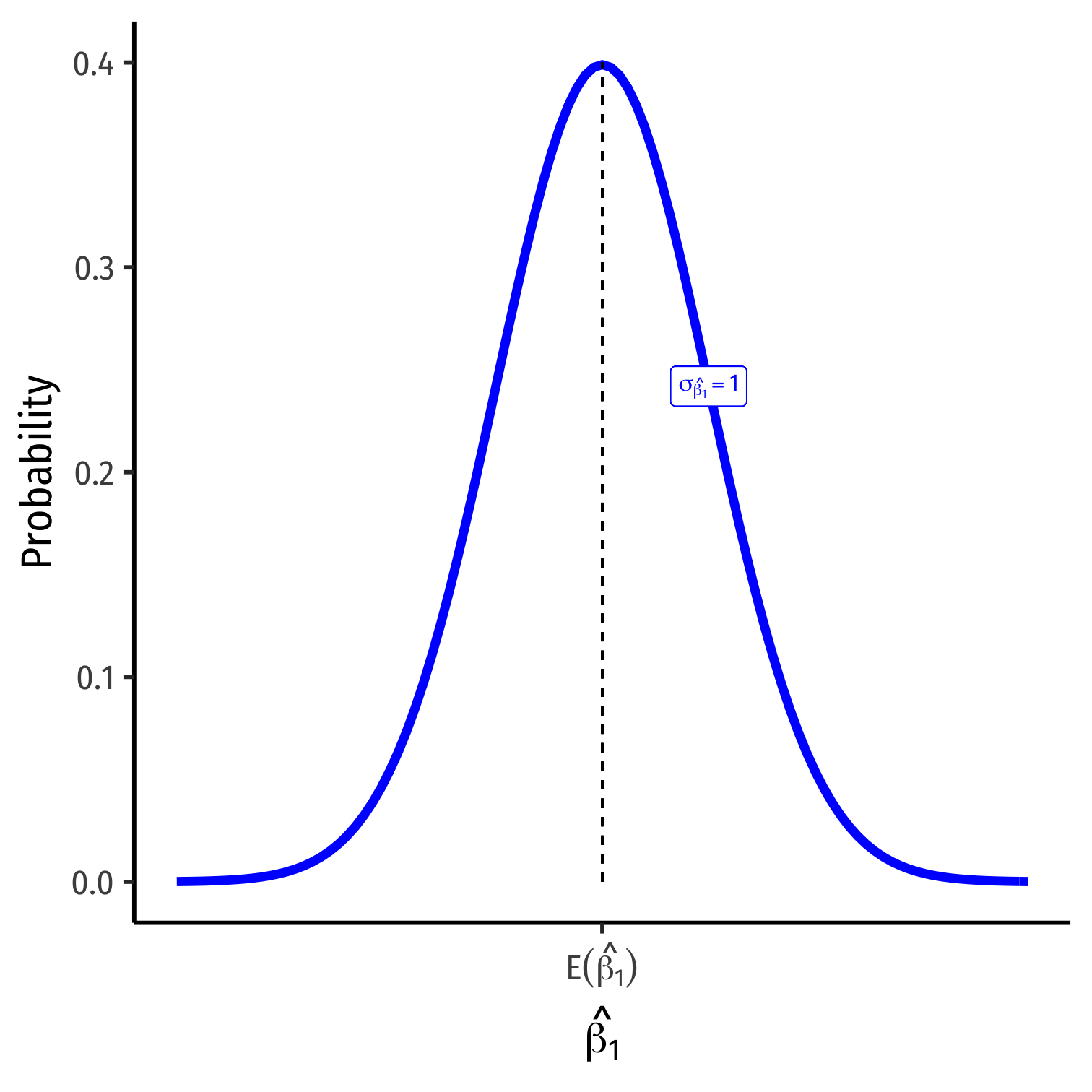

The Sampling Distribution of \(\hat{\beta_1}\)

$$\hat{\beta_1} \sim N(E[\hat{\beta_1}], \sigma_{\hat{\beta_1}})$$

- \(E[\hat{\beta_1}]\); the center of the distribution (last class)

- \(E[\hat{\beta_1}]=\beta_1\)1

The Sampling Distribution of \(\hat{\beta_1}\)

$$\hat{\beta_1} \sim N(E[\hat{\beta_1}], \sigma_{\hat{\beta_1}})$$

\(E[\hat{\beta_1}]\); the center of the distribution (last class)

- \(E[\hat{\beta_1}]=\beta_1\)1

\(\sigma_{\hat{\beta_1}}\); how precise is our estimate? (today)

- Variance \(\sigma^2_{\hat{\beta_1}}\) or standard error+ \(\sigma_{\hat{\beta_1}}\)

1 Under the 4 assumptions about \(u\) (particularly, \(cor(X,u)=0)\).

+ Standard "error" is the analog of standard deviation when talking about

the sampling distribution of a sample statistic (such as \(\bar{X}\) or \(\hat{\beta_1})\).

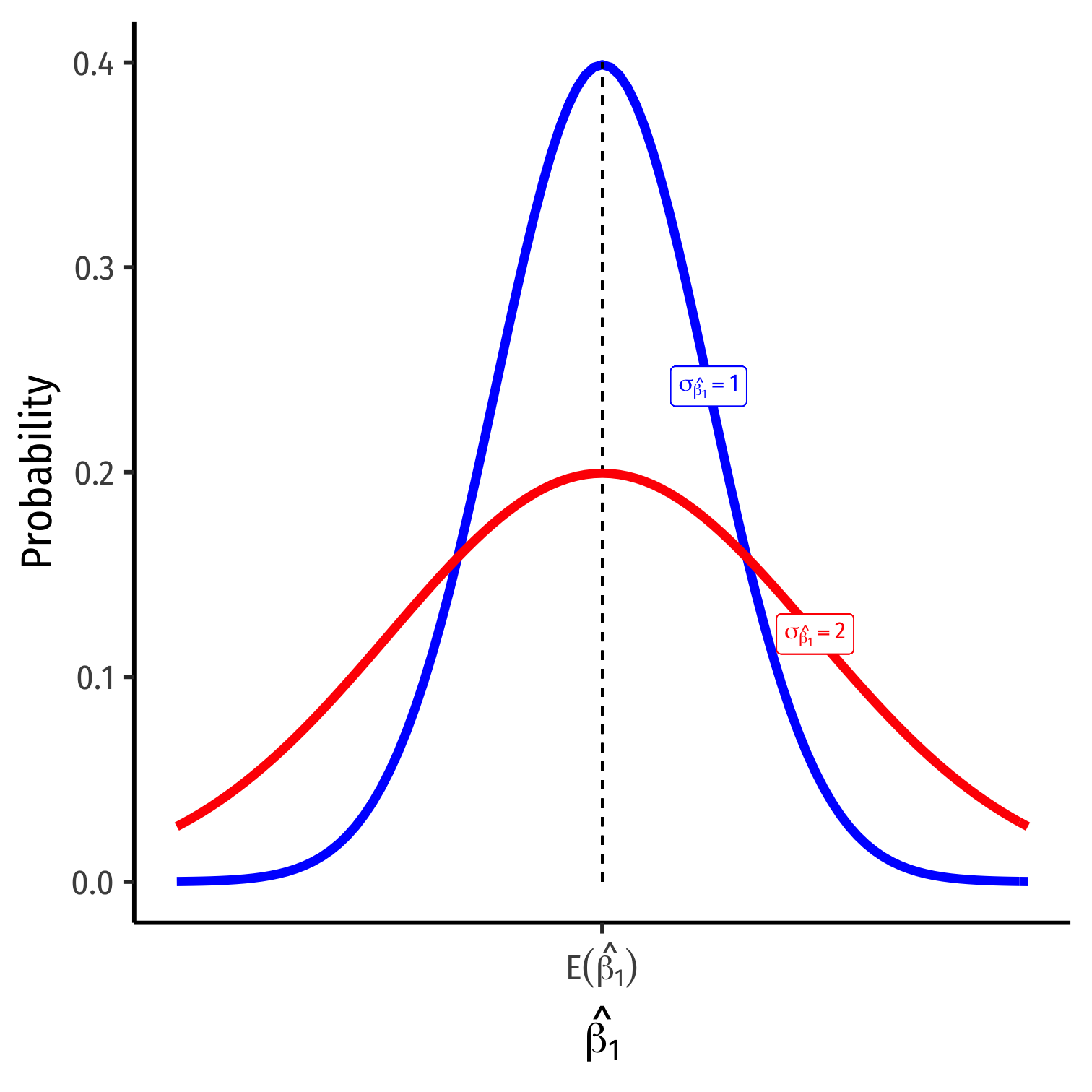

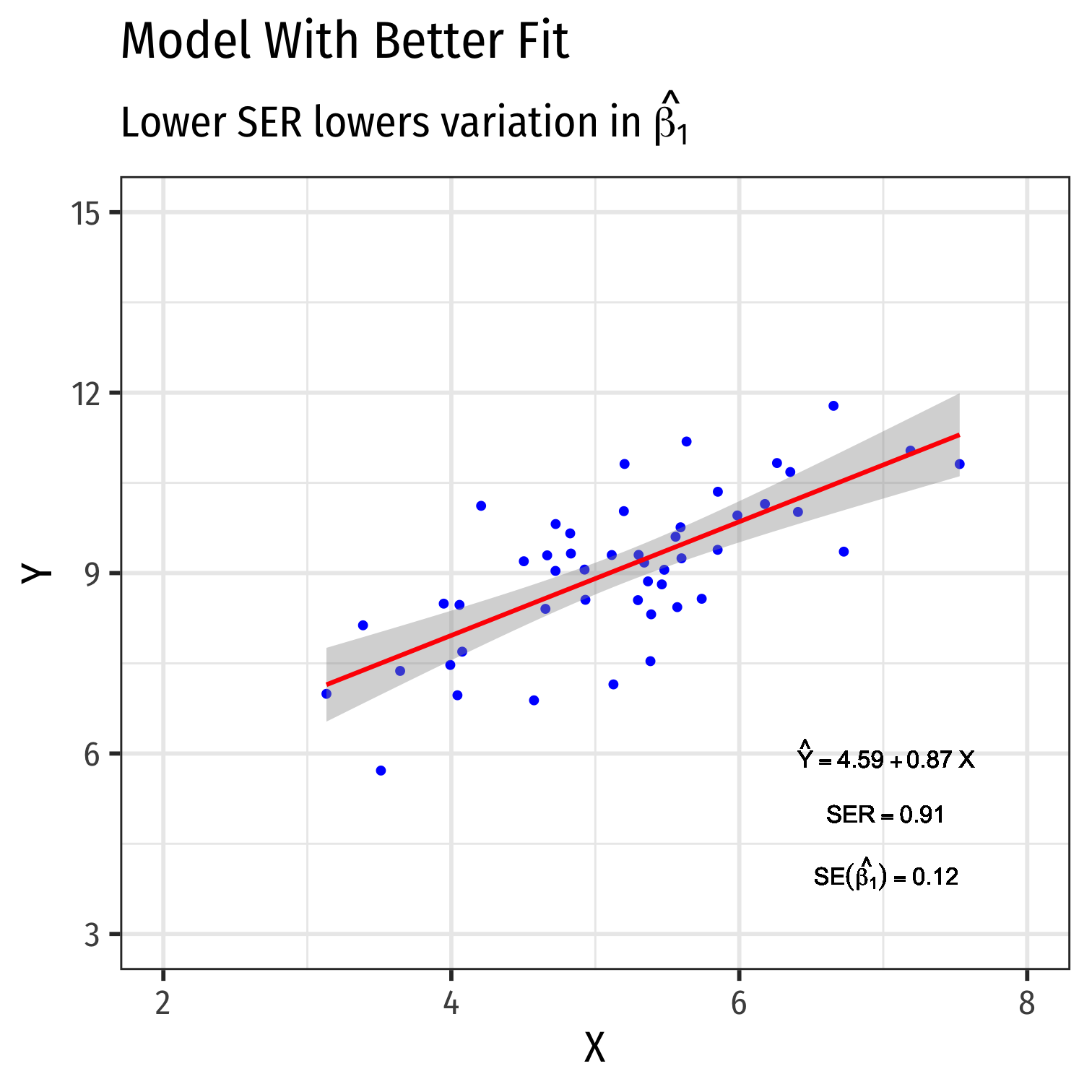

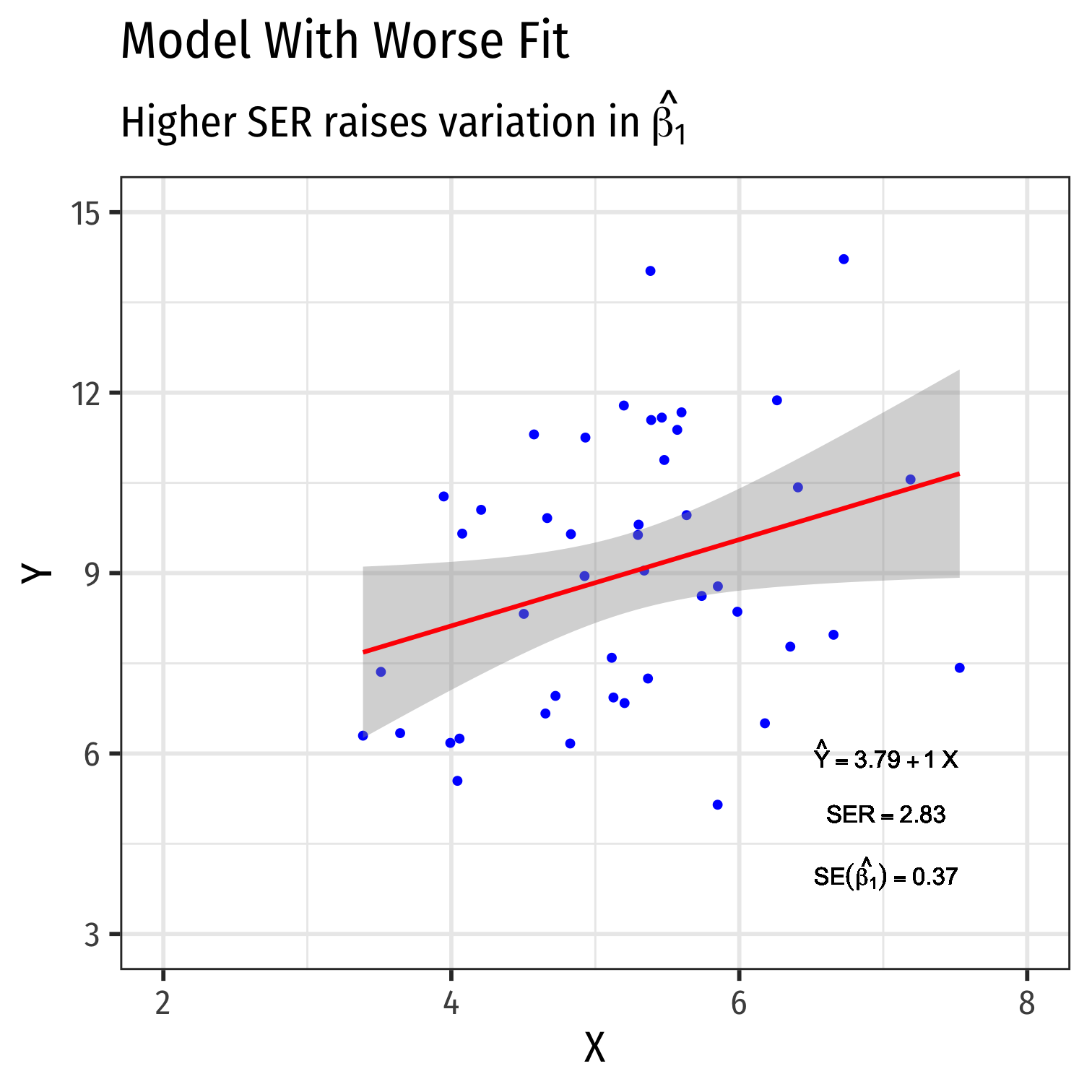

Variation in \(\hat{\beta_1}\): Goodness of Fit

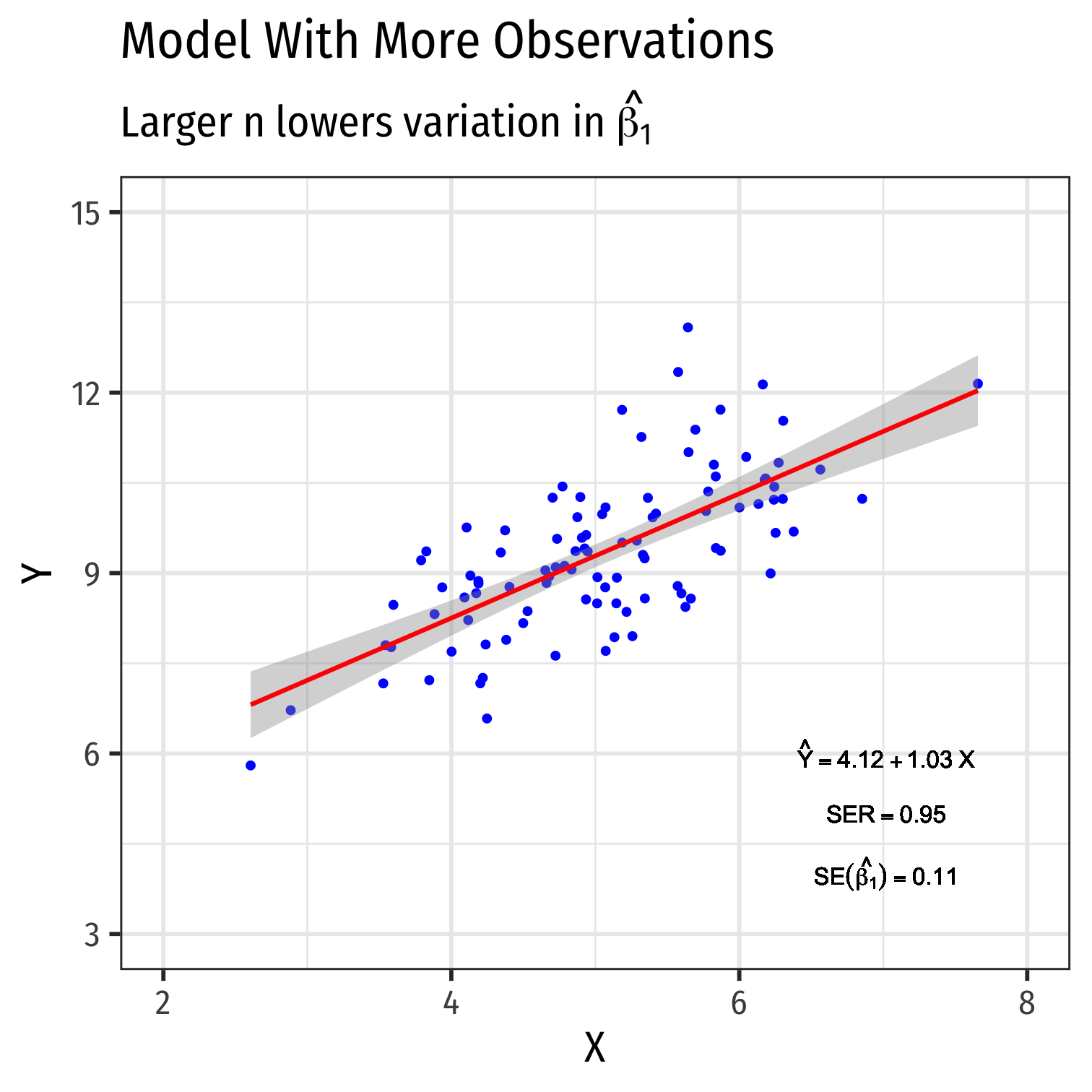

Variation in \(\hat{\beta_1}\): Sample Size

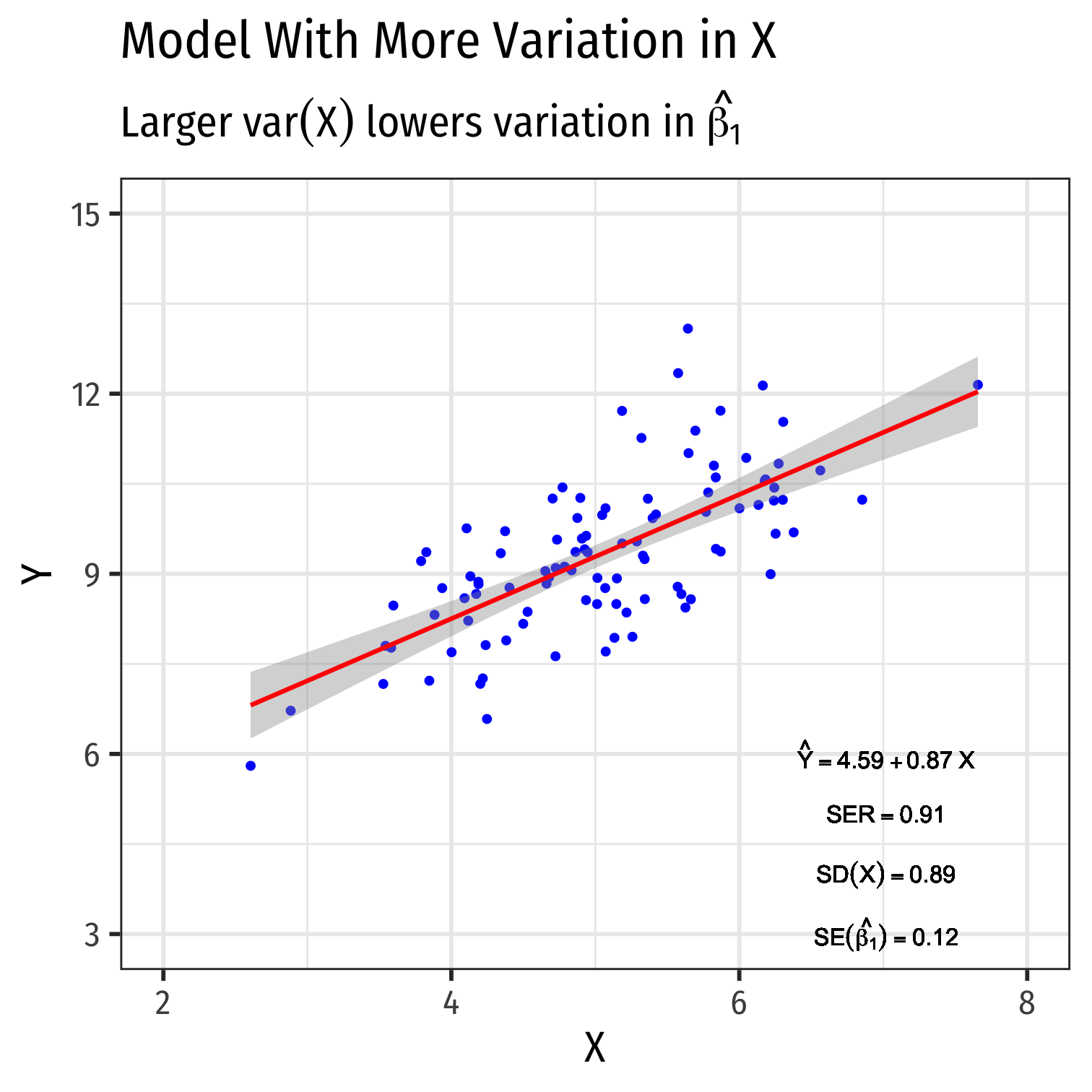

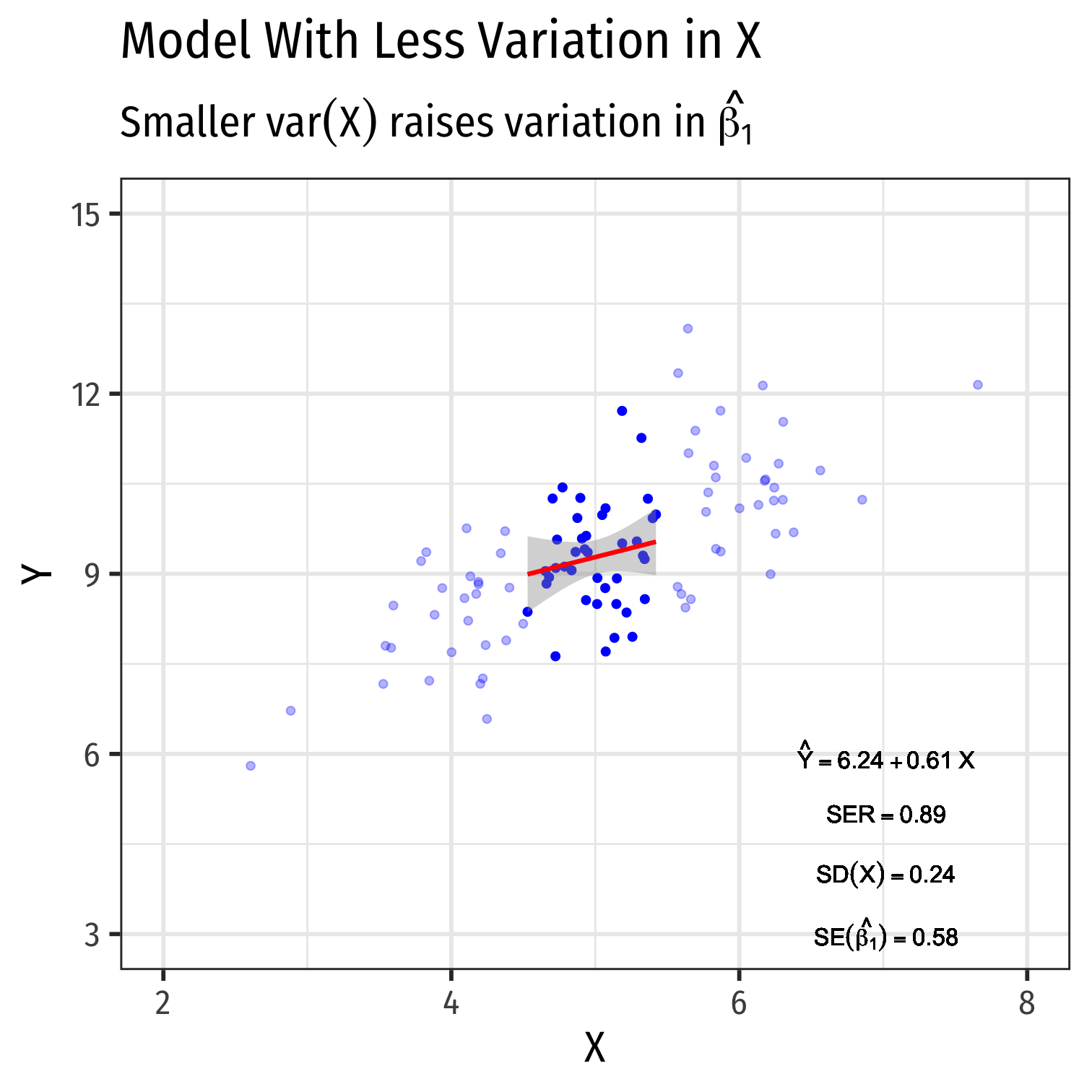

Variation in \(\hat{\beta_1}\): Variation in \(X\)

Recap: Assumptions about Errors

- Recall the 4 critical assumptions about \(u\):

The expected value of the residuals is 0 $$E[u]=0$$

The variance of the residuals over \(X\) is constant, written: $$var(u|X)=\sigma^2_{u}$$

Errors are not correlated across observations: $$cor(u_i,u_j)=0 \quad \forall i \neq j$$

No correlation between \(X\) and the error term: $$cor(X, u)=0 \text{ or } E[u|X]=0$$

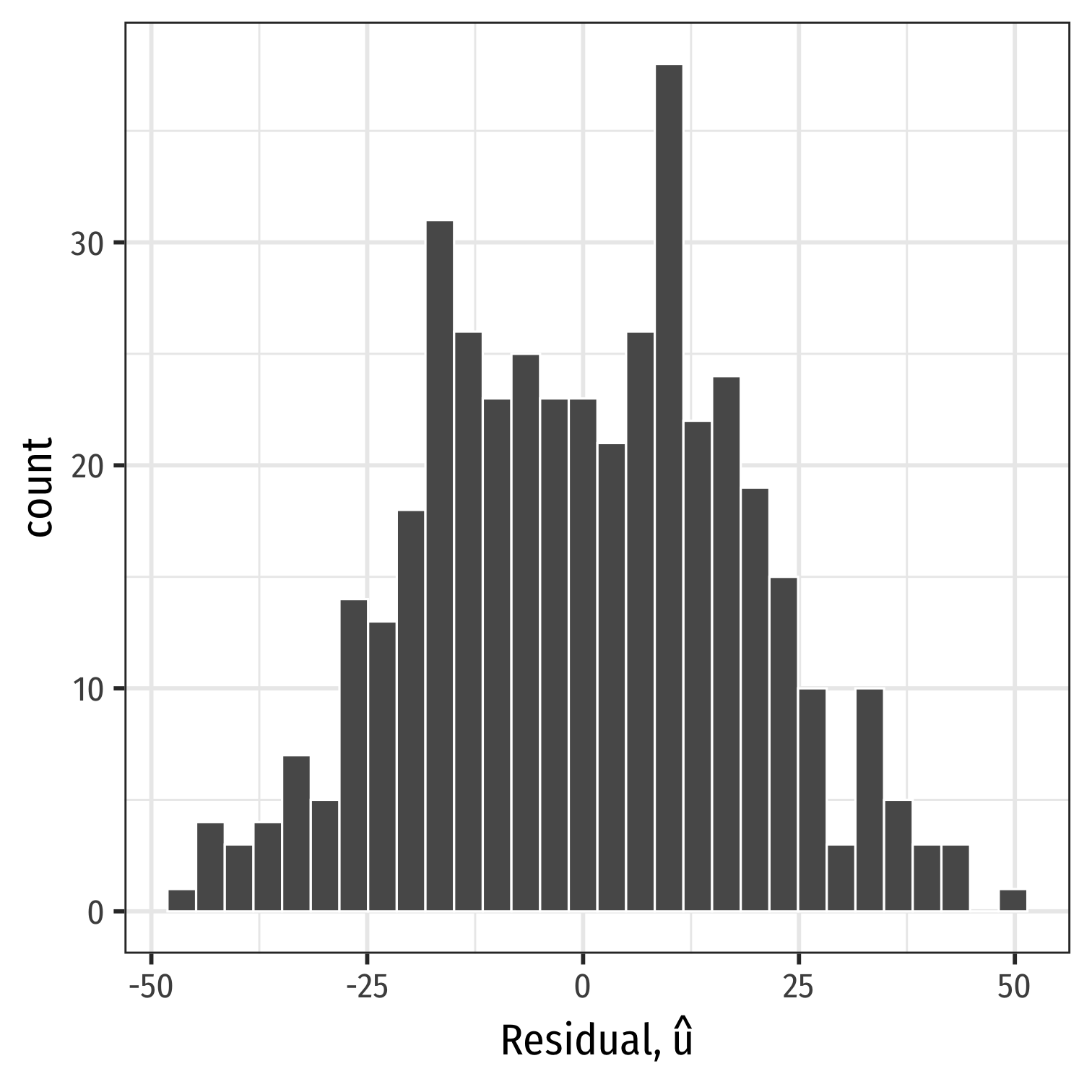

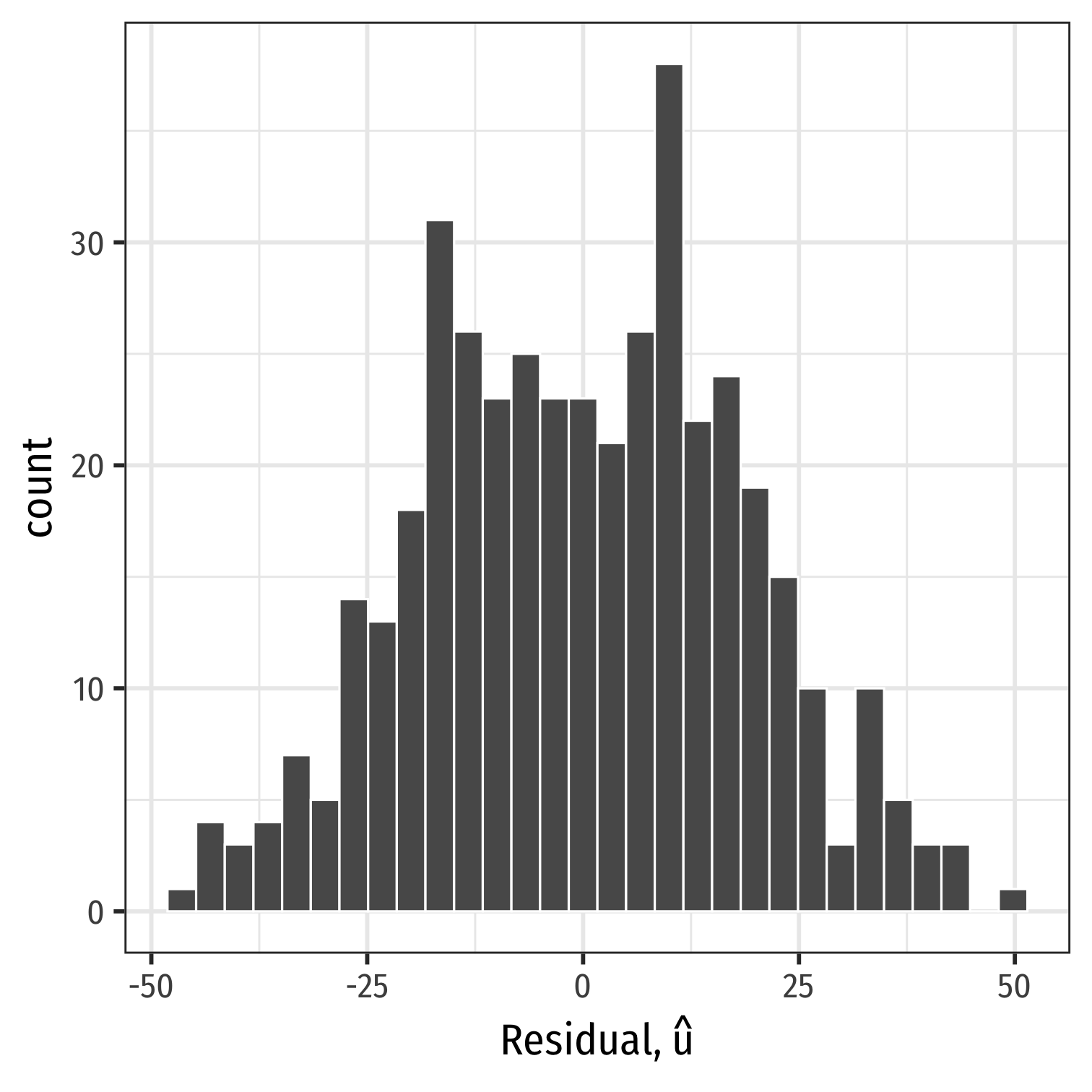

Plotting Residuals

ggplot(data = aug_reg)+ aes(x = .resid)+ geom_histogram(color="white")+ labs(x = expression(paste("Residual, ", hat(u))))+ theme_bw(base_family = "Fira Sans Condensed", base_size=20)

Plotting Residuals

ggplot(data = aug_reg)+ aes(x = .resid)+ geom_histogram(color="white")+ labs(x = expression(paste("Residual, ", hat(u))))+ theme_bw(base_family = "Fira Sans Condensed", base_size=20)- Just to check:

aug_reg %>% summarize(E_u = mean(.resid), sd_u = sd(.resid))| E_u | sd_u |

| -5.76e-16 | 18.6 |

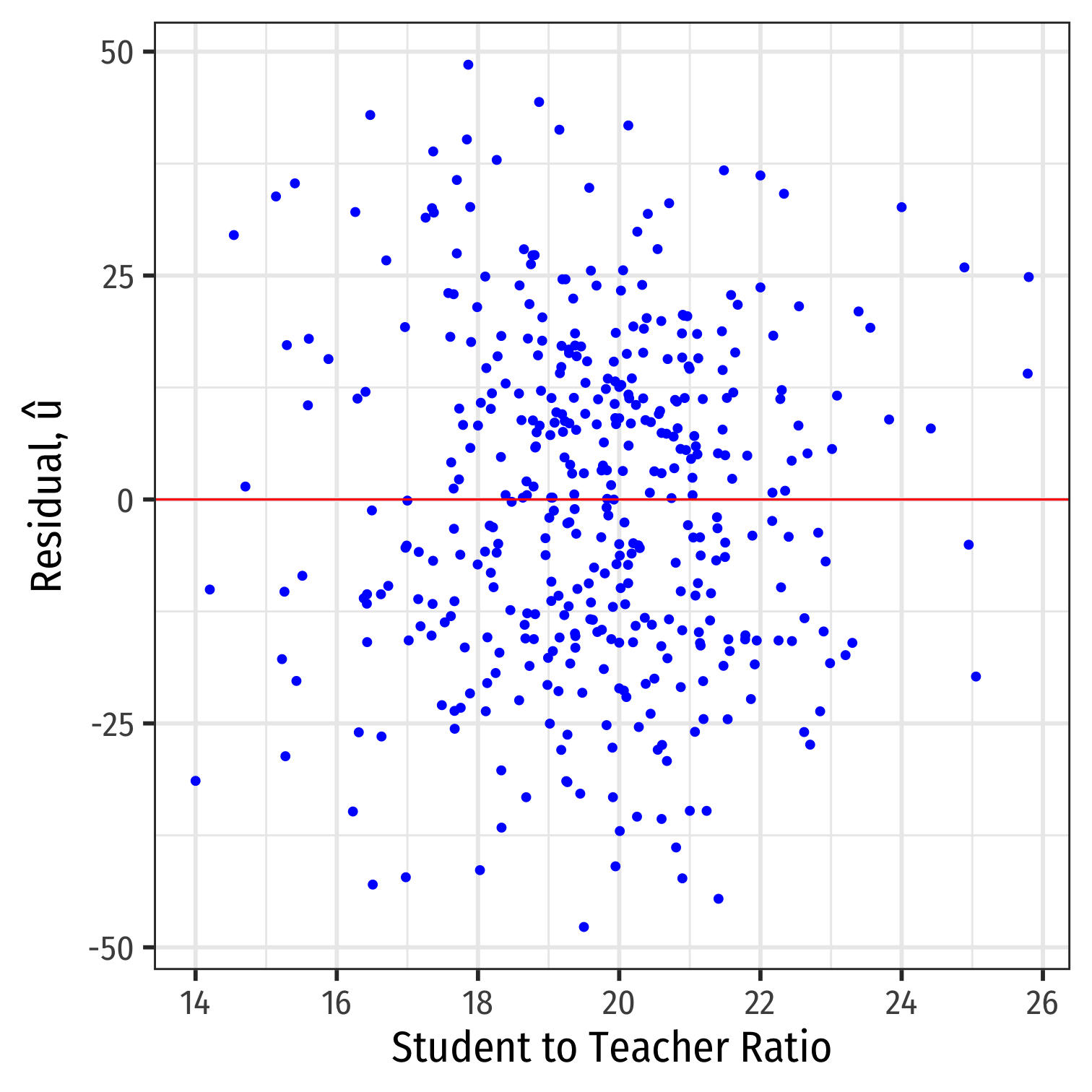

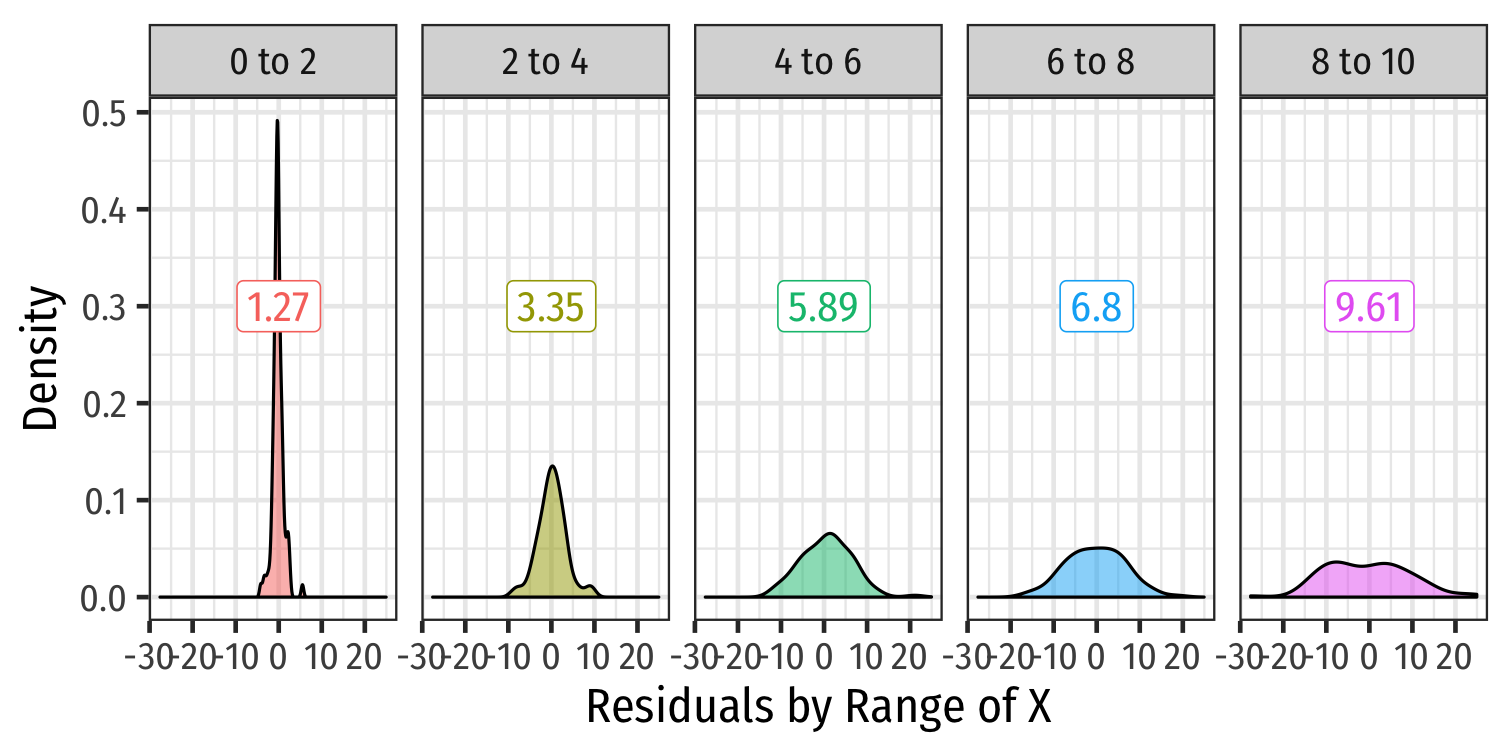

Residual Plot

- We often plot a residual plot to see any odd patterns about residuals

- \(x\)-axis are \(X\) values (

str) - \(y\)-axis are \(u\) values (

.resid)

- \(x\)-axis are \(X\) values (

Homoskedasticity

"Homoskedasticity:" variance of the residuals over \(X\) is constant, written: $$var(u|X)=\sigma^2_{u}$$

Knowing the value of \(X\) does not affect the variance (spread) of the errors

Heteroskedasticity I

"Heteroskedasticity:" variance of the residuals over \(X\) is NOT constant: $$var(u|X) \neq \sigma^2_{u}$$

This does not cause \(\hat{\beta_1}\) to be biased, but it does cause the standard error of \(\hat{\beta_1}\) to be incorrect

This does cause a problem for inference!

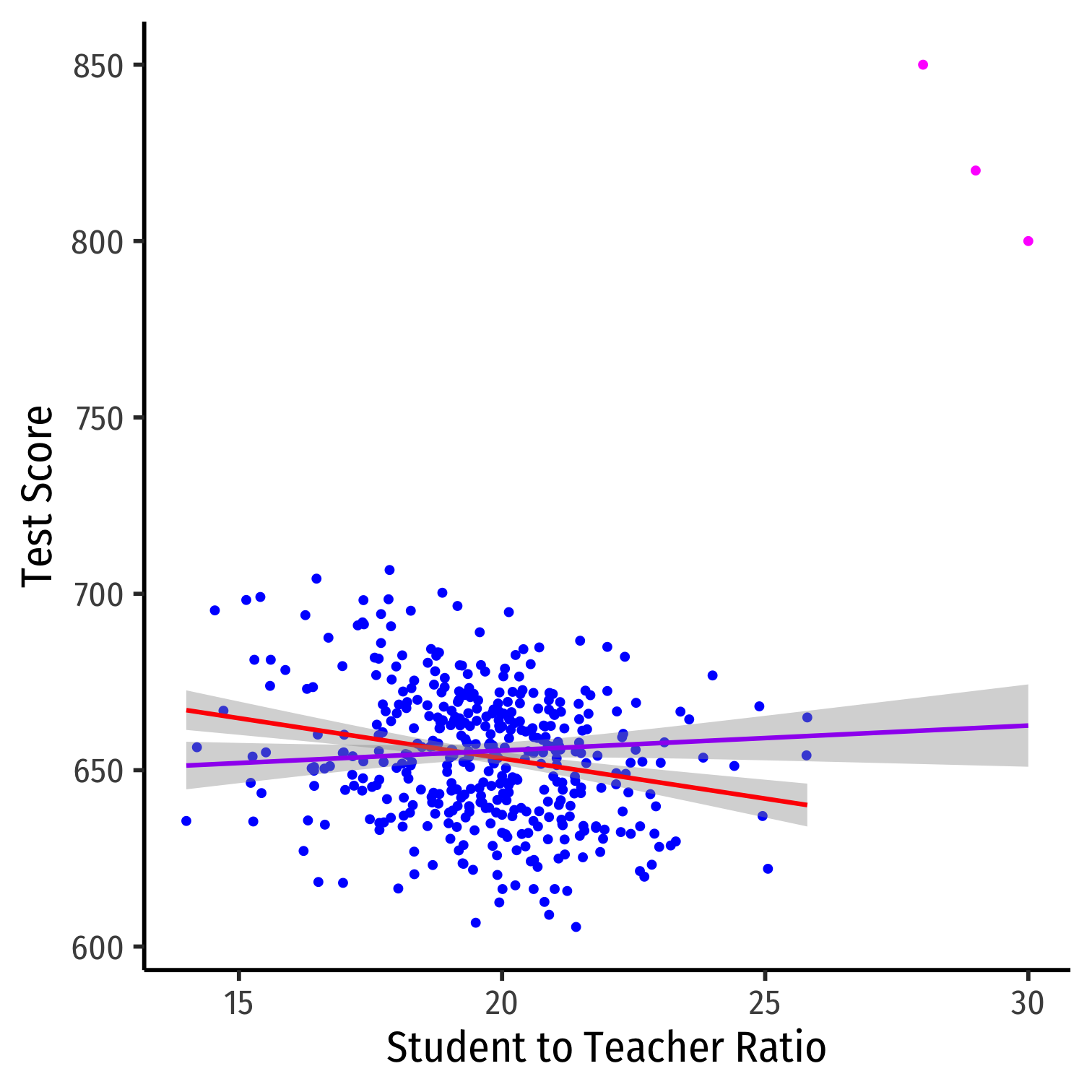

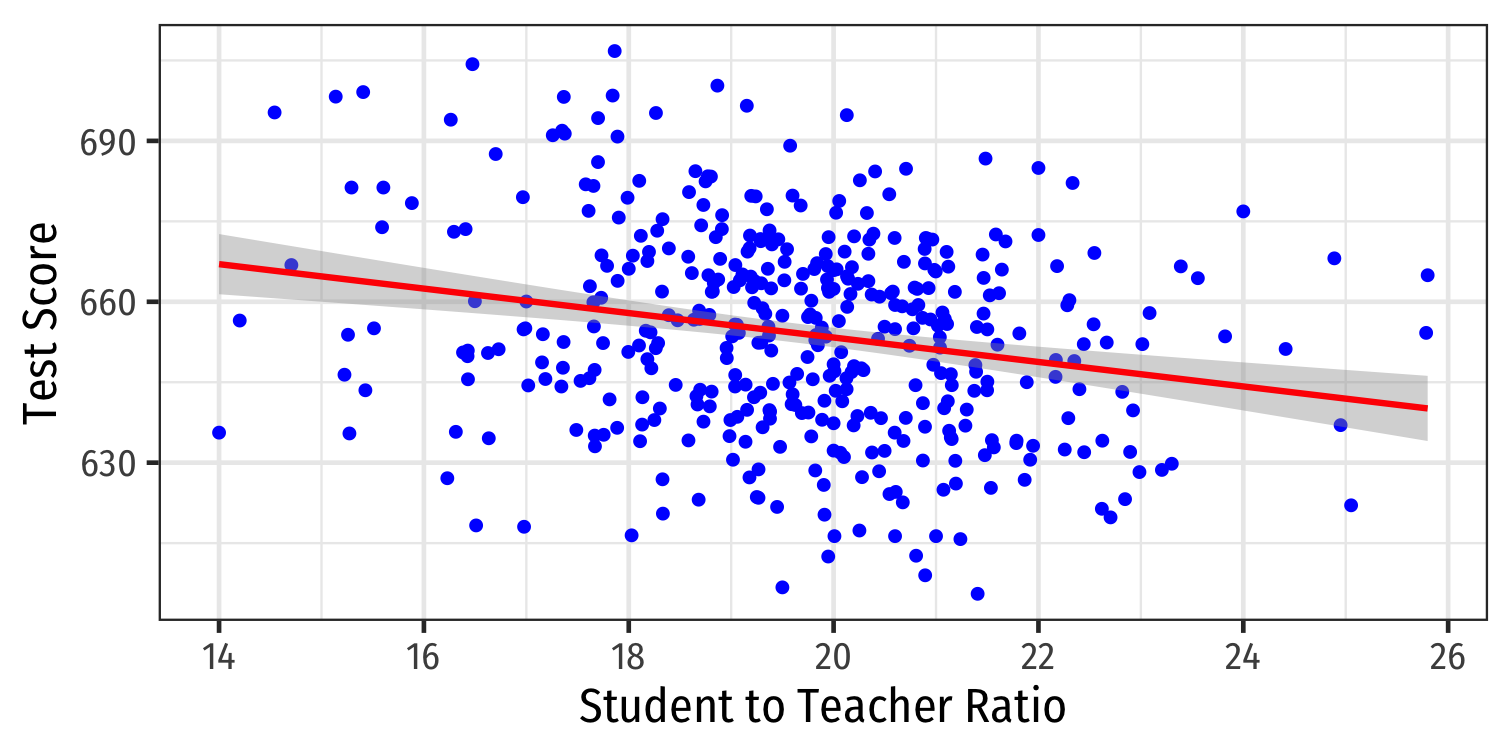

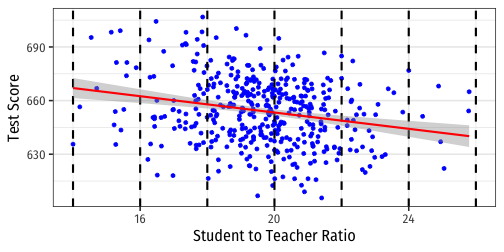

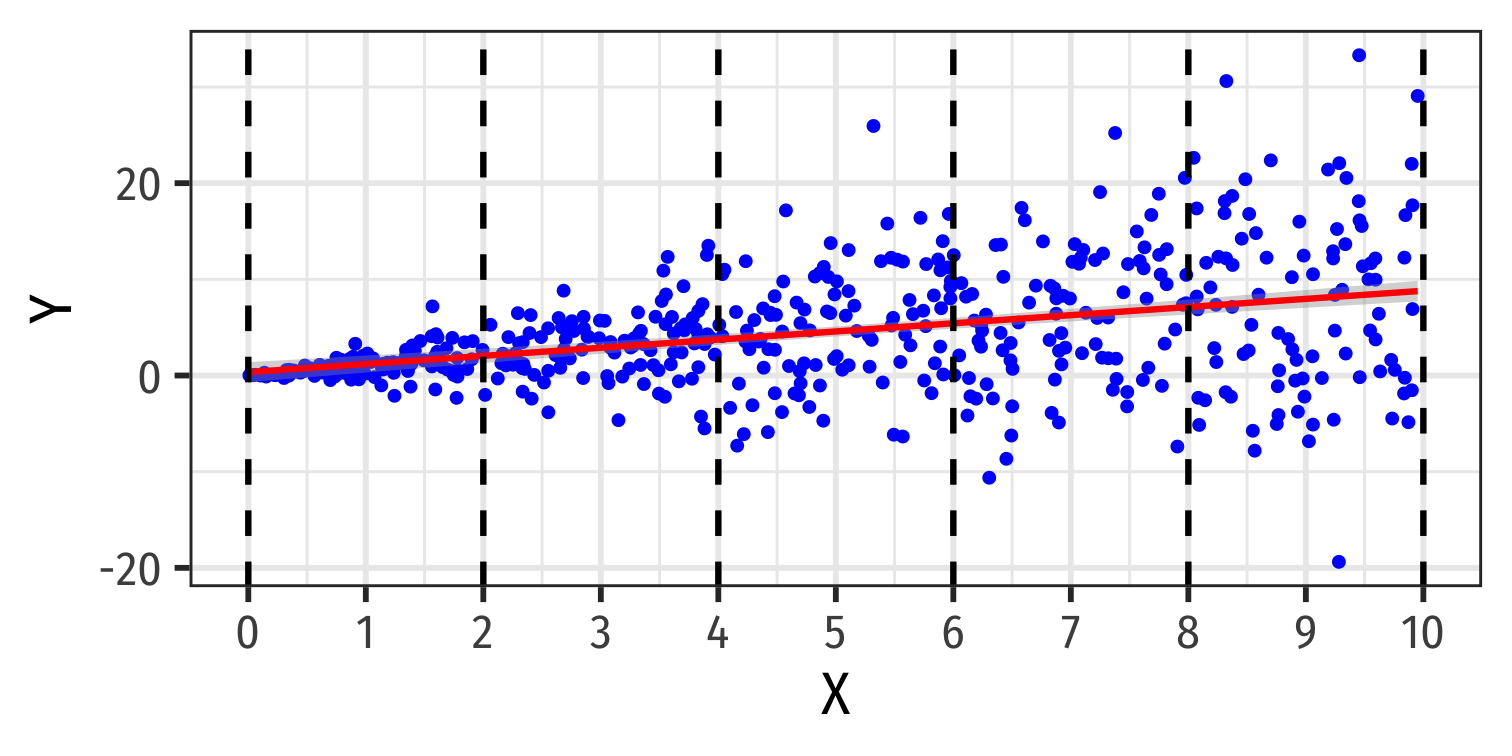

Visualizing Heteroskedasticity I

- Our original scatterplot with regression line

Visualizing Heteroskedasticity I

Our original scatterplot with regression line

Does the spread of the errors change over different values of \(str\)?

- No: homoskedastic

- Yes: heteroskedastic

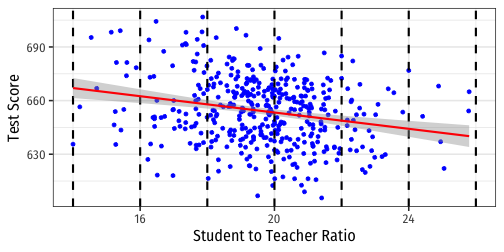

Visualizing Heteroskedasticity I

Our original scatterplot with regression line

Does the spread of the errors change over different values of \(str\)?

- No: homoskedastic

- Yes: heteroskedastic

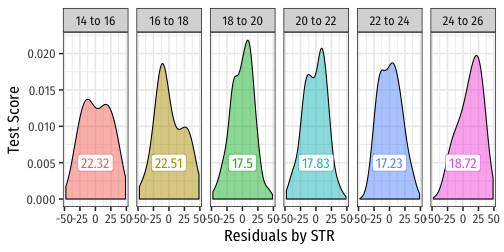

More Obvious Heteroskedasticity

- Visual cue: data is "fan-shaped"

- Data points are closer to line in some areas

- Data points are more spread from line in other areas

More Obvious Heteroskedasticity

- Visual cue: data is "fan-shaped"

- Data points are closer to line in some areas

- Data points are more spread from line in other areas

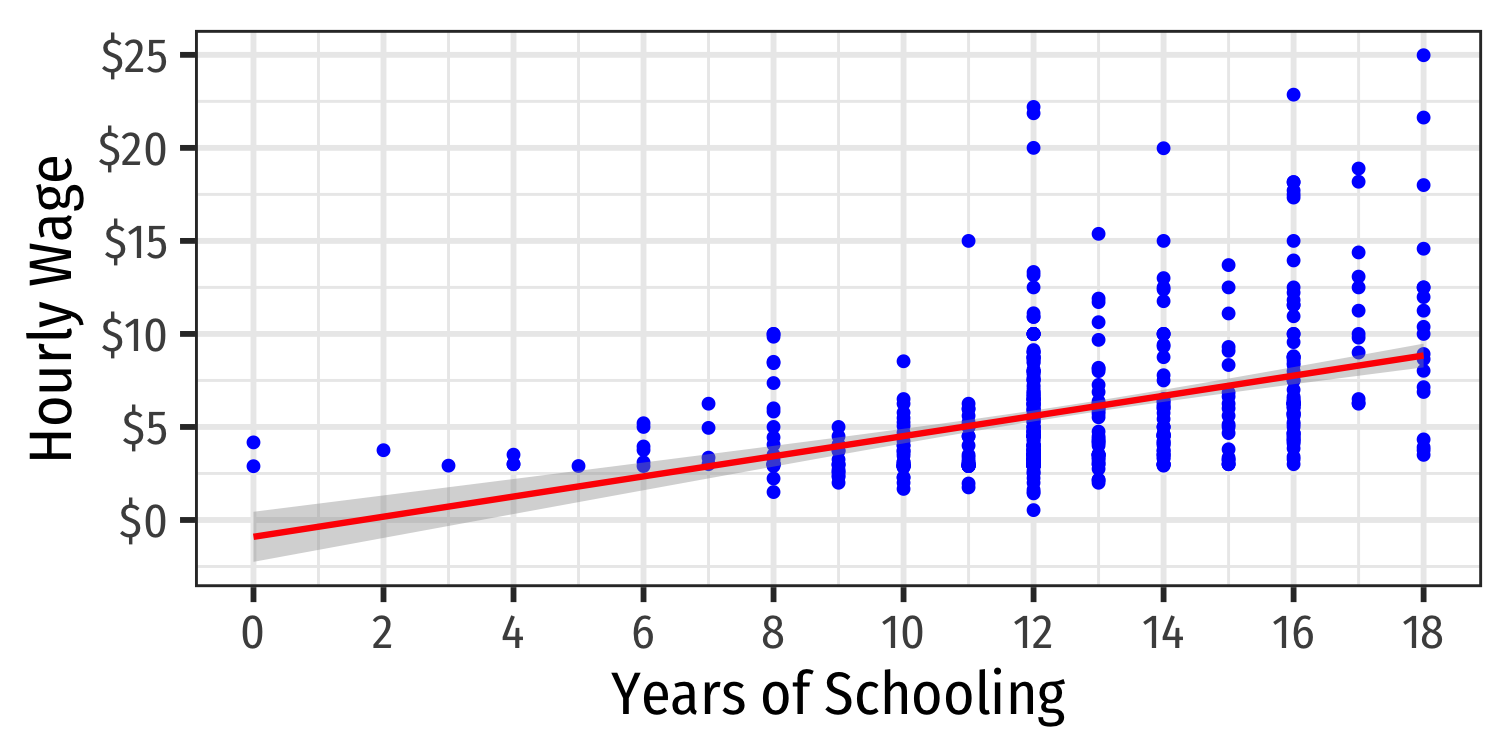

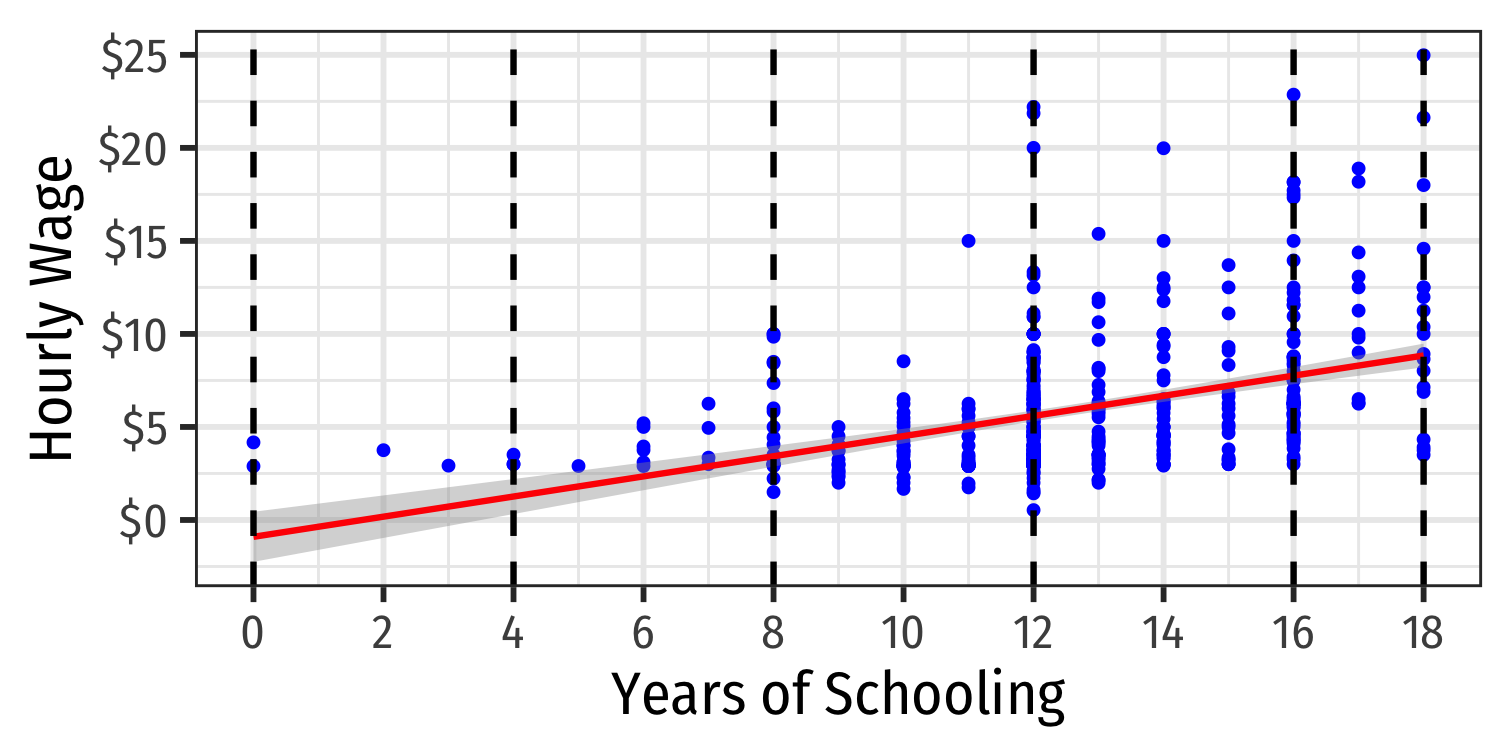

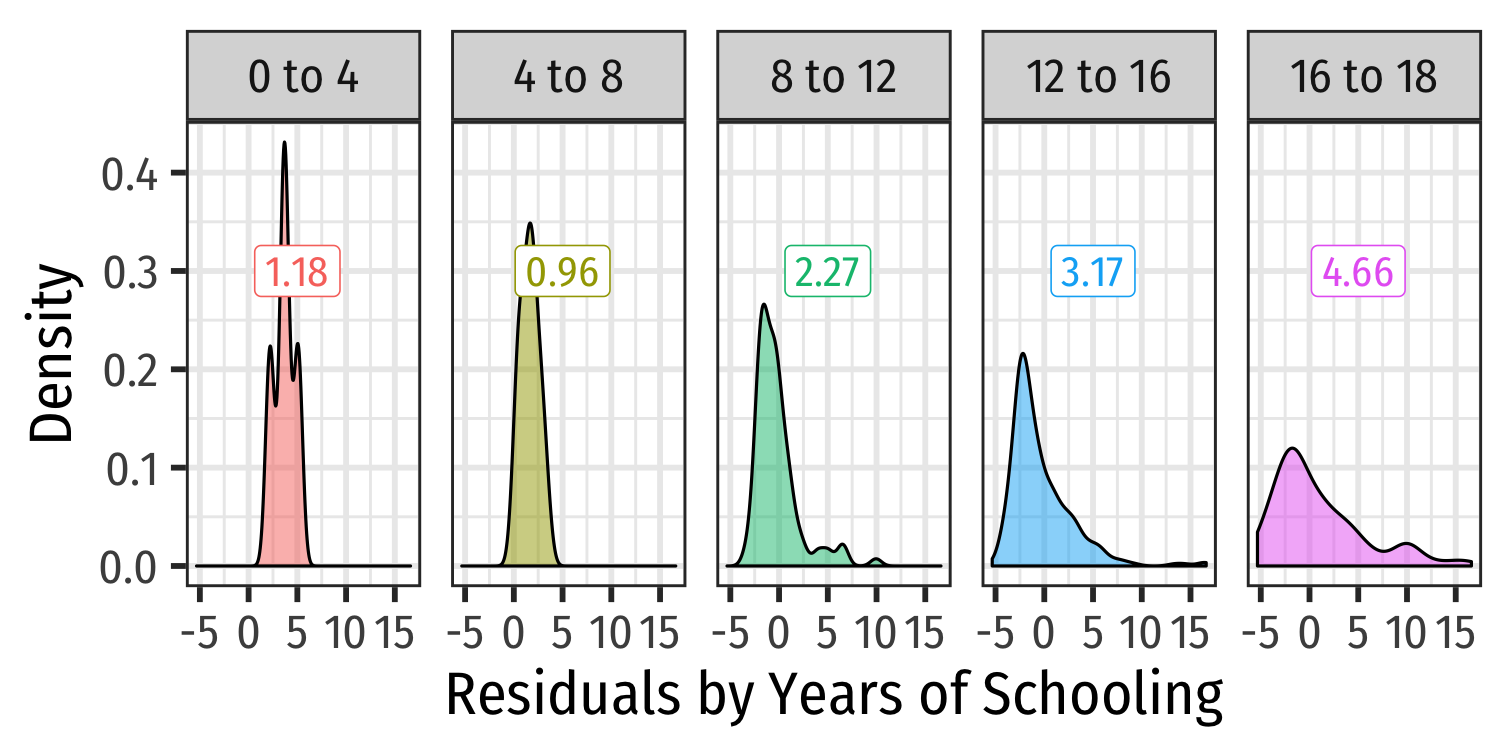

What Might Cause Heteroskedastic Errors?

$$\widehat{wage_i}=\hat{\beta_0}+\hat{\beta_1}educ_i$$

| Wage | |

| Intercept | -0.90 |

| (0.68) | |

| Years of Schooling | 0.54 *** |

| (0.05) | |

| N | 526 |

| R-Squared | 0.16 |

| SER | 3.38 |

| *** p < 0.001; ** p < 0.01; * p < 0.05. | |

What Might Cause Heteroskedastic Errors?

$$\widehat{wage_i}=\hat{\beta_0}+\hat{\beta_1}educ_i$$

| Wage | |

| Intercept | -0.90 |

| (0.68) | |

| Years of Schooling | 0.54 *** |

| (0.05) | |

| N | 526 |

| R-Squared | 0.16 |

| SER | 3.38 |

| *** p < 0.001; ** p < 0.01; * p < 0.05. | |

Assumption 3: No Serial Correlation

Errors are not correlated across observations: $$cor(u_i,u_j)=0 \quad \forall i \neq j$$

For simple cross-sectional data, this is rarely an issue

Time-series & panel data nearly always contain serial correlation or autocorrelation between errors

Errors may be clustered

- by group: e.g. all observations from Maryland, all observations from Virginia, etc.

- by time: GDP in 2006 around the world, GDP in 2008 around the world, etc.

We'll deal with these fixes when we talk about panel data (or time-series if necessary)

Outliers Can Bias OLS! I

Outliers can affect the slope (and intercept) of the line and add bias

- May be result of human error (measurement, transcribing, etc)

- May be meaningful and accurate

In any case, compare how including/dropping outliers affects regression and always discuss outliers!